Public Bank Berhad needs very little introduction. It is a very solid and well manage bank in Malaysia. To continue to fuel its future growth, it has expanded into overseas like Hong Kong, China and fast growing markets like Vietnam and Cambodia. We can a plenty of coverage, so financial data will be very minimum in this entry.

I find it funny watching CIMB's analysts keep calling for neutral or underperfom rating. They were too conservative for too long. Unfortunately or fortunately, Public Bank keeps surprises the market with upsides, till a point no surprise is a surprise. Analysts covering Public Bank behaved like driving by looking at the rear mirror at all times- keep making revisions trailing actual results. If anyone ignored what analysts called and bought in 2003, they already making almost 5 folds return. Why don't we buy this solid blue chip when it has neutral or even underperform rating back then?

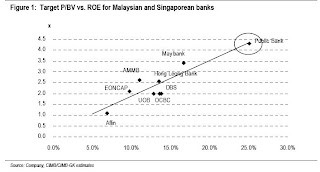

Of late, everyone seems to know it is expensive, based on its 2006 and 2007 financial performance, people are paying almost 4 times book value, more expensive compared to the dizzy days of superbull run. Has Public Bank escalated too much expectations of analysts? Winson Ng of CIMB seems to be cautious in his call in 2007, his guts now grew tremendously, revised his call with much stronger convictions. He was justifying you and I should pay 4 times book value based on its superior ROE of 25%, revised his target from $ 12.7 to $ 14.6 per share. Will he get it wrong this time, putting a cart way ahead of the horse?

Why are people willing to tie their money down on "perceived" undervalued small cap stocks but not Public Bank? Shall we at least allocate small amount of money from our portfolio? Will this so call "limited upside" Public Bank prove everyone wrong again? Will Law of Reversion-To-Mean eventually creep in? I dare not predict the price will fall because it is just too popular. Many fund managers attracted by its good dividend yield and a good alternative to Maybank and CIMB. I am willing to pay for this wonderful business for $ 8-9/share and hold it for a long time.

2 comments:

Turtle, you seems to be a very experienced investor. But in this blog you've only bought MUI so far.

Hi turtle,

Would you please look at Ranhill Utilities and give some opinions.

Thanks

Post a Comment