http://turtleinvestor888.blogspot.com/2008/06/ppbperlis-plantation-berhad-and-wilmar.html

http://turtleinvestor888.blogspot.com/2008/07/ppbperlis-plantation-berhad-and-wilmar.html

http://turtleinvestor888.blogspot.com/2009/02/perlis-plantation-berhad-ppb-update.html

There were 5 risks that I talked about, I re-produce them here

"Risks

1. Collapse of crude oil bring about collapse in soft commodities. It's a low margin business. Net income %: 2003 -- 0.9%; 2004 -- 1.2%; 2005 -- 1.25%; 2006 -- 3.07%; 2007 -- 3.5%. Profitability improvement is due to better economies of scale and also favorable commodity sector.

2. If you trade, the risk of screw up always exist -- involving future, options and etc.

3. Change in government regulations like price control or taxes. Sold down of stock earlier of this year when China government requires them to submit for approval prior to price increase on cooking oil.

4. Weather and natural disasters.

5. Much slower growth ahead via organic growth."

True enough, after smooth sailing of 2.5 years, the got hit in the last quarter. Here is the announcement.

If they trade, I know they will get hit one of these days. Just look at this chart on the volatility of the margin especially in the oilseed and grains segment(this was the culprit of the shocking loss in the last quarter).

When I made a buy call at that time because the risk was low due to the extremely depressed price(RM 9/share). When it has almost doubled, the risk rises tremendously when I have hard times to understand their income statement and balance sheet.

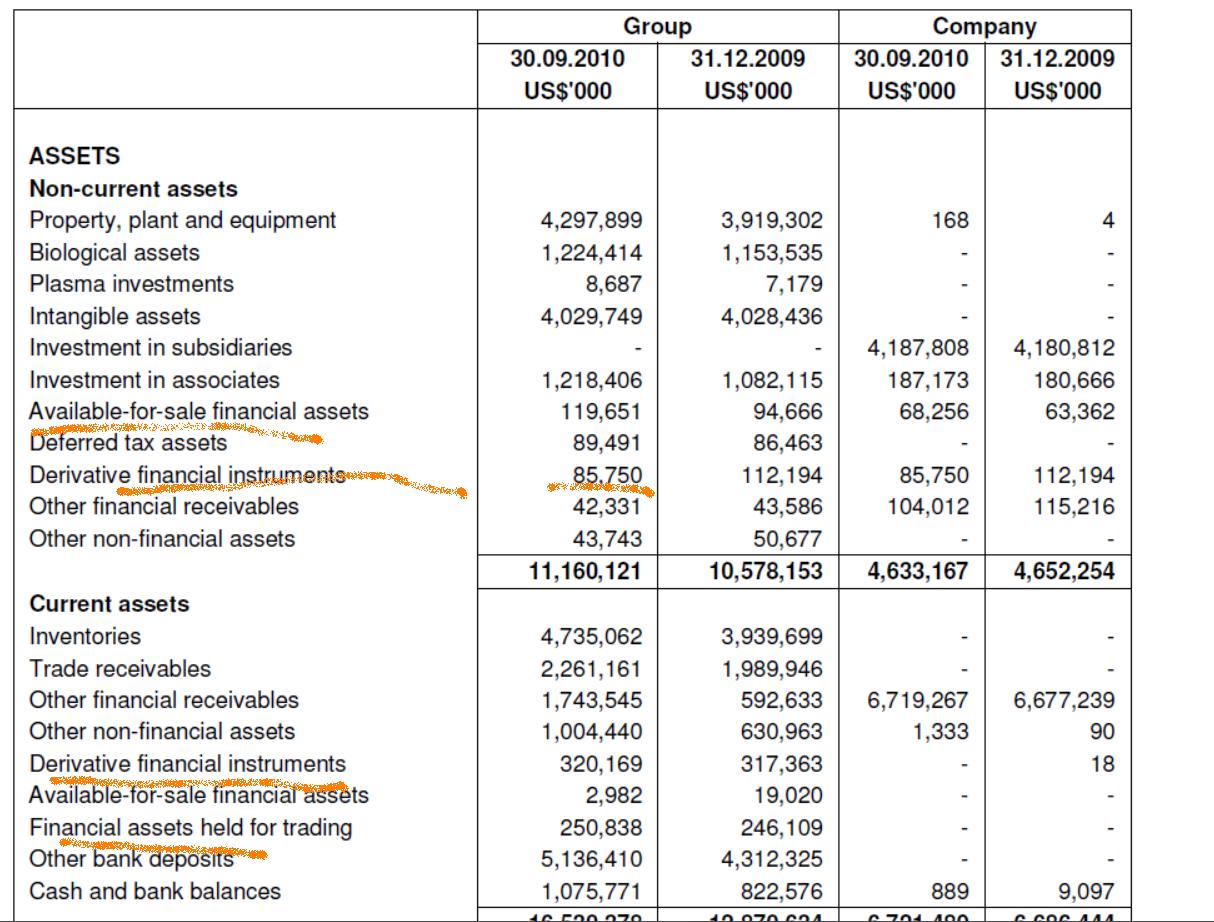

I don't understand the losses on $ 141 million on cash flow hedges.

When you look at their Balance Sheet, you will see $ 300 million Derrivatives here and there. It will make you really headache when you are trying to evaluate the company.

I am not sure how the market will react to this but it is time to take profit and to re-enter again around $ 15 / share.

No comments:

Post a Comment